Disclaimer: Our content is intended to be used and must be used for information and education purposes only. It is very important to do your own analysis before making any investment based on your own personal circumstances.

Once you start to earn money from poker, there are basically three options on what to do with it.

1. Keep it in your poker bankroll.

Up to a point, you need to do this so you can weather the inevitable variance and start taking shots at higher stakes.

2. Withdraw it for expenses.

When playing poker for a living you’ll need to periodically cash out a certain amount to cover expenses. Spending your winnings is a second option that can consist of fixed and variable costs.

3. Withdraw it for savings and investing.

Everyone should be saving to protect themselves against unforeseen surprises in life. You can save more by earning a higher income, or by spending less. Building wealth can be achieved without a high income, but it is nearly impossible without a high savings rate.

The value of wealth lies in offering you options, flexibility, and growth to one day purchase more than you could right now.

– Morgan Housel

Many poker players don’t set aside money from their bankrolls. They’re able to withdraw fast and can move down in stakes if needed.

But having a few months worth in expenses outside your bankroll can be a healthy early financial goal. It can lower your financial stress by allowing you to stay at your stakes even after a losing month or two.

Building wealth has a lot to do with your savings rate. That said, you shouldn’t just save money in cash. Inflation is constantly reducing your money’s purchasing power, and with extremely low-interest rates a savings account is not very appealing either.

That’s why you should consider taking a portion of your poker winnings and look for higher-yielding investments. Think of it as looking for a higher EV play in a poker hand.

Turning Your Poker Winnings Into Wealth

Even though our financial goals are likely to change a couple of times during our lifetime, the goal of investing will remain: to create future wealth.

Would you like to have more flexibility in the future and be in charge of how spend your time? How? With a concept Albert Einstein once said was the eighth wonder of the world.

Compounding

The majority of online poker players are between 20 and 40 years old. The good news is we have time on our side. That’s the most important factor in making maximum use of the compounding effect. Needless to say, it’s important to start sooner rather than later to let time do its work.

The first rule of compounding: Never interrupt it unnecessarily.

– Charlie Munger

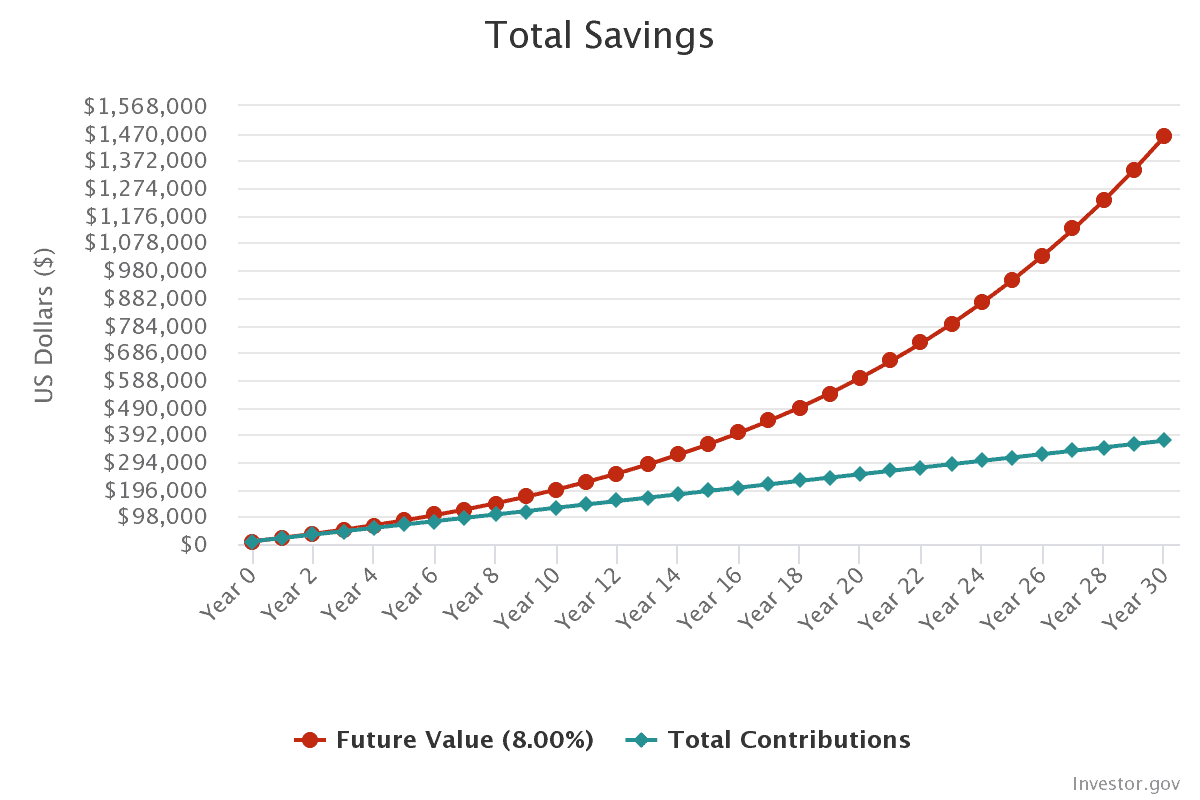

If you start investing today and have this money compound over time it will grow exponentially. In the following graph, we can see that if we invest $10,000 today, contribute $1,000 a month, and assume an annual return of 8% we can see the compounding effect in action.

After 10 years, $130,000 has been contributed and is now worth $195.428, a return on investment (ROI) of +50%. After 20 years an ROI of +138%, and after 30 years an ROI of +294%.

Anyone can start investing today to exploit the compounding effect and let time do the work. In the table below you’ll see the results of starting to contribute on a monthly basis without an initial investment.

Check out this calculator if you’d like to run your own simulations.

As you can see, big financial goals are actually within reach, especially when you’re relatively young. Most family, friends, and fellow poker players have no idea about this crazy compounding effect.

Let’s talk about how we could approach investing as poker players.

Bankroll vs. Investing

As poker players, we basically have two bankrolls, one ‘life-roll’ and our poker bankroll.

The utility of a poker bankroll is to be able to play specific stakes. Based on a certain win rate it determines your hourly earnings rate. The utility of a ‘life-roll’ is to cover expenses, function as an emergency fund, save for marriage or buying a house, or invest to create future wealth.

Managing your finances with only a poker bankroll when it’s the main source of income is risky and can lead to losing financial control. Keeping two bankrolls gives clarity and peace of mind.

Cashing out a certain amount (of your winnings) each month and use it to cover bills, save for a vacation, and/or use for investing, can give you a sense of security, and attach more meaning to why you’re trying to win at poker.

Profiles

If poker is your main source of income, it’s a good idea to cash out a certain amount on a monthly basis. Goals and stakes will be different among players and therefore the amount to periodically cash out is variable.

If you’re using proper bankroll management and have at least 100 buy-ins to play at a particular stake, most of your roll is untouched during a playing month. Of course, we need some backup in case Lady Luck turns her back on us, as downswings will be inevitable.

In the following examples, we’ll focus on which part of the bankroll can be used for investing, based on cash-game stakes.

Low Stakes

The first distinction that should be made for low-stakes players is whether poker earnings are their main source of income. If that’s not the case it’s probably better to set aside money from your main source of income while trying to run up your bankroll.

If you’re playing lower stakes and have the ambition to become a poker pro, it’s best to improve your skill level while increasing your bankroll at the same time. This way, you’re able to play higher stakes in the future and potentially live from poker. With the goal of playing higher stakes, there’s an argument to keep all earnings in your bankroll and keep living expenses as low as possible.

We’ve seen that the compounding effect grows exponentially after time. As a result, it can still be smart to cash out a few buy-ins, even if you have the goal of quickly moving up in stakes. For example, deducting two buy-ins worth $100 has a little impact if you’re a sustainable PLO50 winner, especially keeping around 100 buy-ins in your bankroll.

Mid Stakes

As a mid-stakes player, like for example PLO200 ($1/$2 blinds), you can already make a decent living. There’s more reason for a PLO50 player to keep all buy-ins in his bankroll instead of cashing out to invest. As a PLO200 player, you should definitely make use of the compounding effect and build future wealth.

Even with an aggressive bankroll management style, at least one buy-in worth $200 should be used for investing. Moving up in stakes will now be tougher compared to moving up from the low stakes and swings in results might have a larger impact on your mental state. If you’re a solid winner at PLO200 you might even consider using two buy-ins for investing.

Remember that investing $400 per month with an average annual return of 8% compounds to:

- $69,536 after 10 years, contributing $48,000

- $219,657 after 20 years, contributing $96,000

- $543,759 after 30 years, contributing $144,000

High Stakes

Many players who are active at the highest stakes are playing poker for a living. Successful business people who like to play poker occasionally will generally be losing long-term and are likely to use other sources of income for investing.

If you’re playing $5/$10 blinds it’s already smart to cash out one buy-in worth $1,000. Contributing $1k to index investing on a monthly basis based on an average annual return of 8% will compound to $550,000 after 20 years and making $240,000 in contributions, and even $1,360.000 in 30 years, having contributed $360,000.

At the high stakes, you’re more dependent on good games as other regulars will have an above-average skill level and be continuously trying to improve their game. With edges being smaller, variance will have a bigger impact on your results. That could lead to bigger losing stretches that in return can have an influence on your mental game.

Your Investment Portfolio

The next step is to find the best vehicle that is most likely to give us that sweet long-term return. Some people chase higher returns and some are willing to take extreme risks to achieve it.

Striving for more can become dangerous if you don’t know what you’re doing and start taking on too much risk, especially with money that you cannot afford to lose. It’s the exact same principle as in poker, when someone keeps playing higher stakes until their bankroll takes too big of a hit.

There are many ways to invest. People generally invest in stocks, bonds, real estate, cryptocurrencies, collectibles or a combination of these.

Bonds, especially short-term government bonds or treasury bills, can be used in combination with stocks to offer a margin of safety – however this is more applicable to people nearing their retirement, or cases where preservation matters more than accumulation. Real estate can be quite profitable but it requires a lot of attention and might take a fair amount to start investing in.

Crypto’s track record is certainly not as long as stocks, given Bitcoin was released in 2009. The main cryptocurrencies have certainly had a great return since then, which has led many investment firms to seek having at least some exposure to this asset class. If you’re interested in investing in cryptocurrencies, I’d suggest starting small and educate yourself in how to securely purchase and hold your crypto.

If you are content with a moderately good investment return with low maintenance that is easier to understand, then it’s likely stocks are a better option for your investment portfolio.

Stocks

Anyone can start his investing career today by purchasing shares of a public company, or a group of companies. A share gives you ownership of the corporation relative to the total shares (or company’s stock) outstanding.

Stocks can give that long-term return we’re looking for. This asset class clearly outperformed others like bonds, gold, or cash in the last two centuries.

Stocks have generally more short-term volatility than the other assets but if we invest well-diversified, for the long-term and are able to stay in the game, the risk involved is negligible. Risk to us is either ‘the risk of inadequate return’ which can be overcome by investing long-term, or ‘the risk of permanent loss of capital’.

In poker, variance is the measurement to determine volatility of results. Solid bankroll management should protect us against ‘inadequate returns’ or running under EV. Let’s assume we have a $5,000 bankroll.

If we jump into a $5/$10 game we have 5 buy-ins and run the risk of permanent loss of capital, going broke. This is clearly a high-risk situation. When we decide to start playing $0.25-$0.50 games we have 100 buy-ins to work with. This way we minimize risk.

Stocks will function best as the cornerstone of our investment portfolio given their relatively high reward and because we’re able to reduce the risk to a minimum in a similar way as in the example. We can even exploit inadequate returns (dropping stock prices) but more on that in the Contributions section. First, let’s look at investment strategies.

Strategies

When investing in stocks, two basic strategies can be followed: active or passive investing. Passive investors execute a strategy by following the market and letting time do the work. Such investors are index trading and happy with the return the market is offering.

On the other side are the active traders. These investors believe in outperforming the market’s return by actively buying and selling stocks.

- Active investors use stock-picking and/or market timing techniques to actively seek future winning stocks thereby trying to outperform the market’s return

- Passive investors follow a long-term ‘buy-and-hold’ strategy with just a few transactions and are happy with the return the market is offering

Studies show that the large majority of active investors aren’t able to beat the “buy-and-hold” strategy. Many active investors buy and sell at the wrong time, they buy into euphoria or sell when there’s bad news and the stock valuation is cheap. They also tend to pay more fees. You can read more about the advantages or disadvantages of both in this Investopedia article.

Horizon

People aim to earn the highest returns but it’s more important to earn good returns that can be repeated over a long time horizon. When the power of compounding comes into play investments will grow exponentially.

In order to make great use of the compounding effect, we should aim for a 20-year horizon or even longer. Choosing such a long horizon will also help deal with volatility and bring its dispersed short-term returns back to the average, history has taught us.

US stocks (aka businesses) have historically produced an expected annual return of 8% on average. If we assume inflation is 2% in a given year where our stocks return us 8%, our purchasing power return is 6%. On the other hand, saving money by putting it under our pillow will decrease its value by 2%.

Costs

Until now, we’ve only seen the compounding effect in relation to gross returns, thereby excluding costs. If we compare the costs of passive index funds with actively managed funds though, we’ll find another strong reason to follow a passive strategy for a significant part of our investment portfolio.

Let’s assume an investment of $50,000 with a 30-year horizon and an annual return of 8%. When it’s invested in an index fund, costs are around 0.5% per year. Fees of active funds vary and were approximately 2% in the early 00’s. These days it’s more like 1.5% and we’ll take this number to illustrate the point.

The initial investment using a passive strategy has grown to $437,748 while the active fund is returning only $330,718. A seemingly small difference of 1% in yearly costs compounds into a difference of $107,030 after three decades! This results in a return after thirty years of more than 30%, following a passive strategy that aims to minimize costs and not without reason.

Vehicles

Now we know that a significant part of our investment portfolio should be built on a long-term passive strategy, let’s look into the two main options: index mutual funds and Exchange-Traded Funds (ETFs).

- An Index fund is a mutual fund type that consists of the same shares as a specific benchmark index such as the S&P 500 in order to match its performance, not outperform.

- ETFs consist of a basket of assets and can track an index but also a particular industry or commodity. ETFs can be traded at exchanges throughout the day where index funds will only be priced and therefore eventually traded once a day.

Costs associated with both vehicles are different and have their own (dis)advantages. Make sure to check it out to make the optimal decision on which vehicle to choose.

Players should be index investing to create future wealth during their poker journey. The strategy is easy to understand and execute. Its value is based on historical evidence, low in costs, saving a lot of time, and is less confusing.

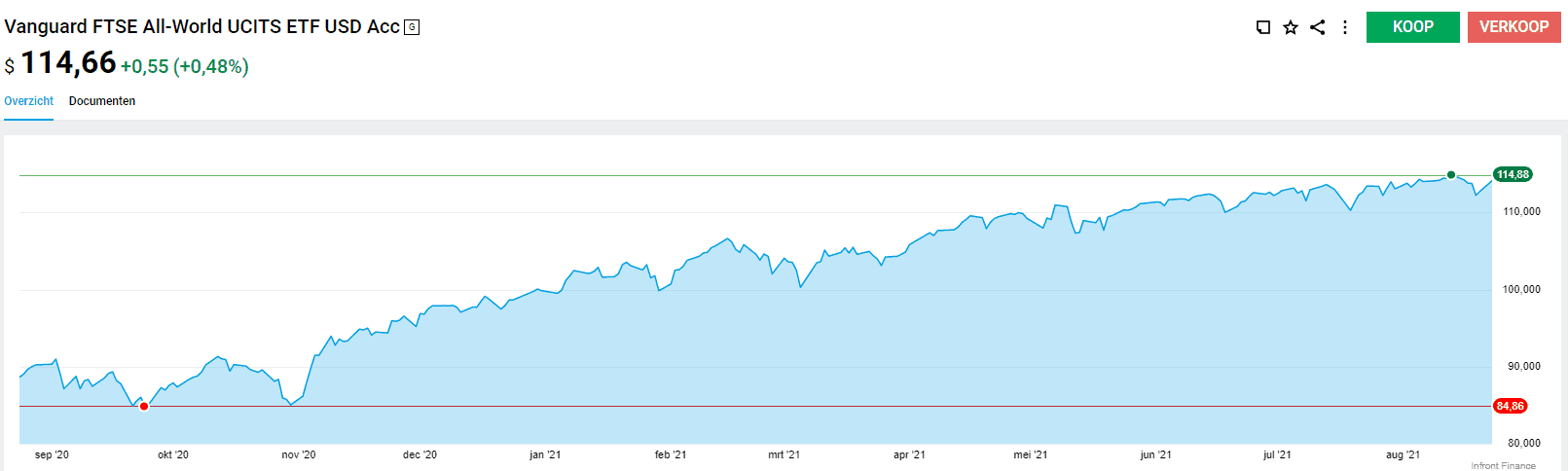

One example of an ETF that invests in companies across the world is the Vanguard FTSE All-World UCITS ETF USD Acc.

Contributions

A basic investment technique that has become very popular is Dollar-Cost Averaging (DCA). DCA means investing equal amounts at regular time intervals. The goal of DCA is to reduce the impact of volatility on the total investment. For example, instead of investing $5,000 in one go, making 25 smaller investments of $200 per month, despite the market price.

If you’d have the opportunity to invest $50,000 today and the market collapses 30% next month, it can have an impact on our well-being, even realizing it’s the winning strategy long-term.

Executing a periodic investing or Dollar-Cost Averaging strategy can counter feelings of regret or anxiety to even start investing, and even protect against short-term risk. It can help achieve your long-term financial goals in a disciplined and practical way. Some banks allow you to set up an automatic DCA strategy, so once you set it up, you don’t have to worry about it anymore.

Conclusion

We’ve seen how the utility of money is different for a poker player. There’s more discipline necessary when playing poker for a living. Managing your finances with only one bankroll can decrease financial control over time and in extreme cases leave you broke.

Consider your financial goals, the asset allocation of your investment portfolio with its associated risk, and make sure it’s in line. To what extent index investing plays a role, you decide.

The goal is to find the cornerstone asset that gives us the best chance of long-term wealth creation.

If you’re new to investing and personal finance, a great book to start is “The Psychology of Money”, by Morgan Housel. It covers a wide variety of topics that will help you in your financial journey, and it’s an enjoyable read on top!

Hopefully, there’s value in this article for you. It would’ve been nice if I knew this information while playing high stakes myself in the early 2000s since I would be compounding for over 15 years already.

I hope other poker players can work on a safe(r) financial situation, being in control and able to create future wealth for themselves, and their families.